TI continues domination of analog IC market

29 May 2013

News

Information from Databeans

Worldwide economic uncertainty has given the analog IC market plenty of ups and downs over the last several years; however 2012 was one of the worst years for this segment.

Analog was down 7% from 2011 with revenues just shy of $40 billion, although this was the unfortunate reality for the entire semiconductor market, which suffered an average decline of 3% in 2012.

All markets within analog did poorly, with the exception of the wired market. Power, automotive and communications were the most resilient, whereas computer, interface and data conversion products took the worst hit.

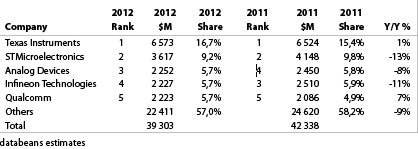

Texas Instruments remains the largest manufacturing company in analog in terms of market share; they finished 2012 with 16,7% of the entire market, or $6,6 billion in revenue. The company’s 2011 acquisition of National Semiconductor has proven to be a very profitable purchase as its market share in interface jumped from 23% to 27% and analog power IC share went from 21% to 24% in 2012.

With TI’s recent decision to restructure its business, it has been able to focus its efforts more on its dominance of the analog market. TI remains resilient, despite the oversupply in the industry caused primarily by China’s slowing economy and the ongoing debt crisis in Europe.

STMicroelectronics remained the second largest in market share for 2012 at slightly over 9% and $3,6 billion in revenue. Like TI, STMicroelectronics is attempting to better allocate its resources in the midst of a poor market and is dissolving its joint venture with Ericsson to better focus its efforts in analog products and power management. Being Europe’s top chipmaker, the firm is likely facing similar oversupply problems and other issues regarding the European economy.

Analog Devices makes up the third largest market share at 5,7% and $2,3 billion, but saw a year-over-year decline of 8%. It currently has the largest market share in the data converter segment, making up half of the market with $1,1 billion in 2012 revenue.

The overall data converter market was down for all companies by an average of 14%; however ADI only took a 12% decrease and the company’s market share increased slightly from 2011. Within the data converter market, ADI easily has an 84% share in high-speed ADCs and a 60% share in overall ADC revenue, making it the worldwide leader in both segments.

For more information visit www.databeans.net

Further reading:

Rooibos heads to space

News

A South African scientific initiative linking agriculture and space research has officially launched today with the Rooibos in Space programme at Parklands College’s Innovation Centre in Cape Town.

Read more...

From the editor's desk: Local can be international

Technews Publishing

Editor's Choice News

Welcome to the July 2026 issue of

Dataweek. As you can see from this introduction,

Dataweek’s regular editor, Peter Howells, is on extended leave and I am filling the void in his editor’s column – hopefully without being too boring.

Read more...

Landis+Gyr EMEA introduces new company name: EYKON

News

EYKON is the new company name of Landis+Gyr EMEA, formerly part of the Landis+Gyr Group. The company supports electricity, gas, water and thermal utilities in managing increasingly complex networks, improving operational efficiency and enabling more sustainable use of resources.

Read more...

Yamaha Robotics will show visitors to EFX

Manufacturing / Production Technology, Hardware & Services News

Yamaha Robotics will show visitors to EFX 2026, the Expo for Electronics Manufacturing, in Stuttgart from 6-8 October 2026, how advanced surface-mount automation helps companies grow their business and increase productivity.

Read more...

From the editor's desk: The art of measuring the truth

Technews Publishing

Editor's Choice News

All electronic measurements are a lie. The trick is making the lie as small as possible.

Read more...

TSE has relocated

News

The Technology Station in Electronics (TSE) has entered a new chapter with its relocation from the CSIR campus to TUT-owned building at Ditsela Place in Hatfield.

Read more...

Innovative MyLegrand app

RS South Africa

News

Legrand SA is set to launch the MyLegrand mobile application, a digital platform designed to strengthen engagement across its professional network.

Read more...

Kulani Energy acquires critical assets from Optipower

News

Kulani Energy preserves engineering, procurement, and construction capability and positions a wholly women-owned firm at the forefront of South Africa’s grid expansion.

Read more...

From Cape Town to Johannesburg

News

Würth Elektronik South Africa has taken a significant step forward with its recent relocation from Cape Town to Johannesburg, marking a new phase of growth and ambition for the company.

Read more...

Lesley Havenga: Building partnerships for Africa’s electronics future

Editor's Choice News

As Würth Electronik expands its footprint across South Africa and the broader sub-Saharan region, Havenga’s blend of manufacturing expertise, supply chain knowledge, and people-centred leadership appears well suited to the task.

Read more...

printer friendly version

printer friendly version