Global semiconductor revenues fell by 2% in 2015, as sequential quarterly growth was weak throughout every quarter of the year, especially in the first when the market declined 8,9% over the previous quarter – the deepest sequential quarterly decline since the semiconductor market collapsed in the fourth quarter of 2008 and first quarter of 2009.

Global revenue in 2015 totalled $347,3 billion, down from $354,3 billion in 2014, according to IHS. The market drop follows solid growth of 8,3% in 2014 and 6,4% in 2013. “Weak results last year signal the beginning of what is expected to be a three-year period of declining to stagnant growth for semiconductor revenues,” said Dale Ford, vice president and chief analyst at IHS Technology. “Anaemic end-market demand in the major segments of wireless communications, data processing and consumer electronics will hobble semiconductor growth during this time.”

Overall semiconductor revenue growth will limp along at roughly 2,1% compound annual growth rate (CAGR) between 2015 and 2020, according to the latest information from the IHS Semiconductors Service. Current technology, economic, market and product trends suggest that sometime between 2020 and 2022, new products will come to market that will enable a significant level of growth in semiconductor revenues.

Reshaping the leader board

“Of course the big story for the semiconductor industry was the record level of merger-and-acquisition activity last year,” Ford said. “Top players pursued bold, strategic manoeuvres to enhance their market position and improve overall revenue growth and profitability.”

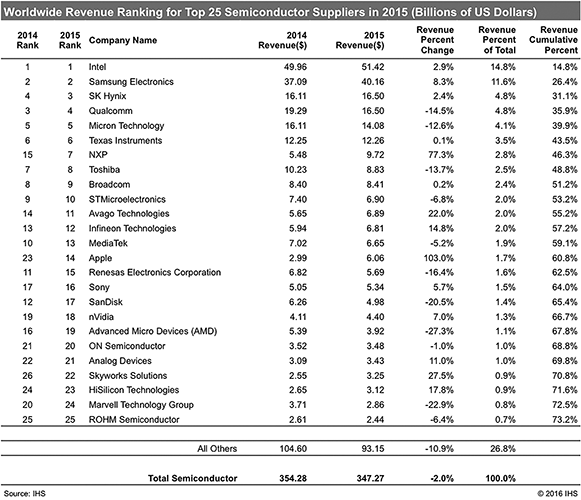

Intel retained its number one ranking in 2015, after completing its acquisition of Altera, which allowed the company to offset declining processor revenues and achieve 2,9% overall growth in 2015. Qualcomm slipped to number four in the rankings as its revenues fell by 14,5%, because the company’s 2015 acquisition of CSR was not enough to counter declining revenues in the wireless markets. The final major deal among the top 10 in 2015 was NXP’s acquisition of Freescale, which boosted it from number 15 in the 2014 rankings to number 7 in 2015.

Among the top 20, Infineon’s acquisition of International Rectifier enabled it to jump to number 12 in 2015. Announced deals that are expected to close in the first half of 2016 will continue to reshape the leader board. Avago Technologies continues its aggressive acquisition activity with its purchase of Broadcom, which is already ranked at number 9 in 2015. The combined revenues of the two companies would place them at number 5 overall. ON Semiconductor’s acquisition of Fairchild Semiconductor should boost it up 2 notches in the rankings.

Among the top 25 semiconductor suppliers, 14 companies achieved growth in 2015. This stands in sharp contrast to the overall semiconductor market where less than 42% of 285 companies tracked by IHS were able to achieve positive revenue results in 2015.

A reversal of fortunes

Whereas 2014 was a year of broad-based strength and growth, the market downturn last year left few markets unscathed. Semiconductor revenues for data processing, wired communications and consumer electronics all declined. Automotive electronics and industrial electronics grew less than 1%, while wireless communications – the strongest growth area – only grew 3%.

Semiconductor revenues in all regions of the world declined, and all seven of the major semiconductor segments (i.e., memory integrated circuits (ICs), microcomponents, logic ICs, analog ICs, discrete components, optical components and sensors) experienced revenue declines from 2014 to 2015. In fact, out of 128 semiconductor segments and sub-segments tracked by IHS, 89 declined. Combined, these 89 segments accounted for over 77% of semiconductor revenues in 2015.

In 2014, five of the six semiconductor end-market segments grew; only consumer electronics declined. All regions, except Japan, achieved revenue growth and 88 out of 128 semiconductor segments and sub segments accounted for over 83% of semiconductor market revenue growth.

In 2014, 195 of 307 companies tracked achieved positive growth. These companies accounted for 83% of total semiconductor market revenues. The number of companies achieving growth in 2015 fell to 119 out of 285 companies tracked. These 119 companies only accounted for 64% of total semiconductor market revenues.

The few bright glimmers from 2015

Only 10 semiconductor market sub-segments worth more than $1 billion in annual revenue grew more than 5% year over year in 2015. Wireless communications logic application-specific integrated circuits (ASICs) and analog ASICs both grew 30%, while radio-frequency (RF) small signal transistors, wired communications logic ASICs and wireless communications application-specific standard products (ASSPs) grew between 10% and 20%.

For more information about the IHS Semiconductors Service, contact the sales department at IHS in the Americas at (844) 301-7334 or americasleads@ihs.com; in Europe, Middle East and Africa (EMEA) at +44 1344 328 300 or technology_emea@ihs.com>; or Asia-Pacific (APAC) at +604 291 3600 or technology_APAC@ihs.com.

For more information visit www.ihs.com

© Technews Publishing (Pty) Ltd | All Rights Reserved

printer friendly version

printer friendly version